However certain royalty income earned by a non-resident person may be exempted from tax. IMoneymy Learning Centre All Categories.

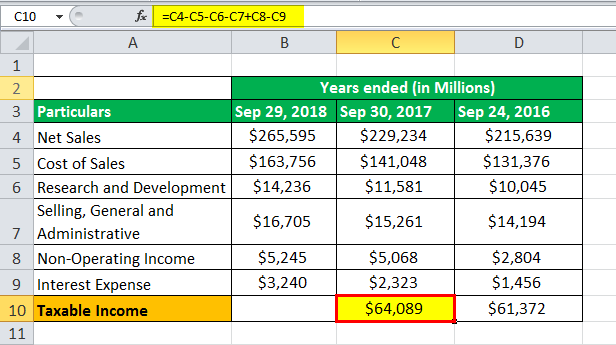

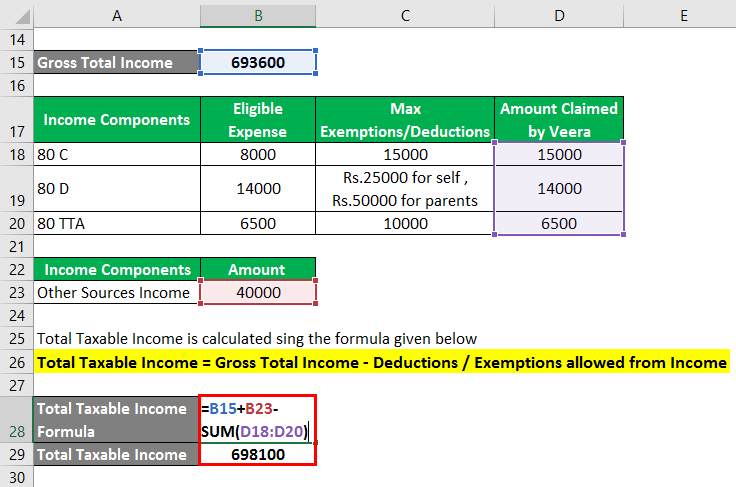

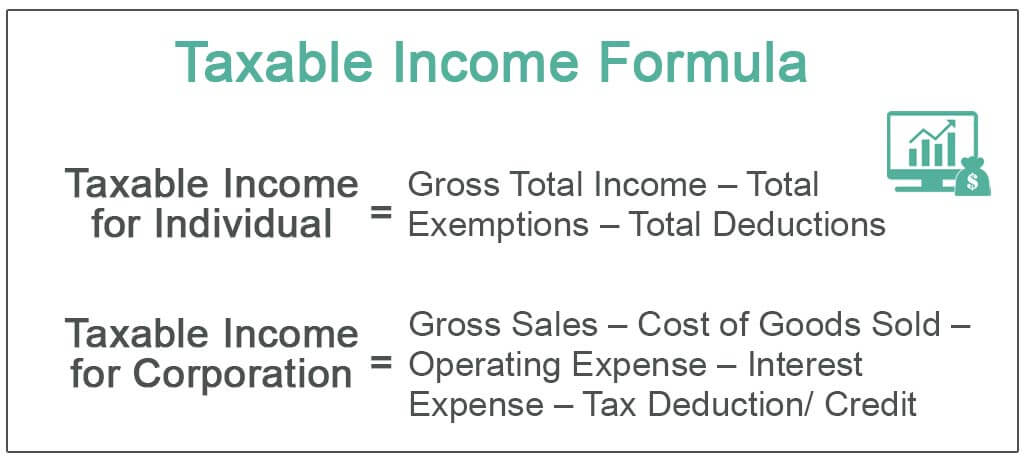

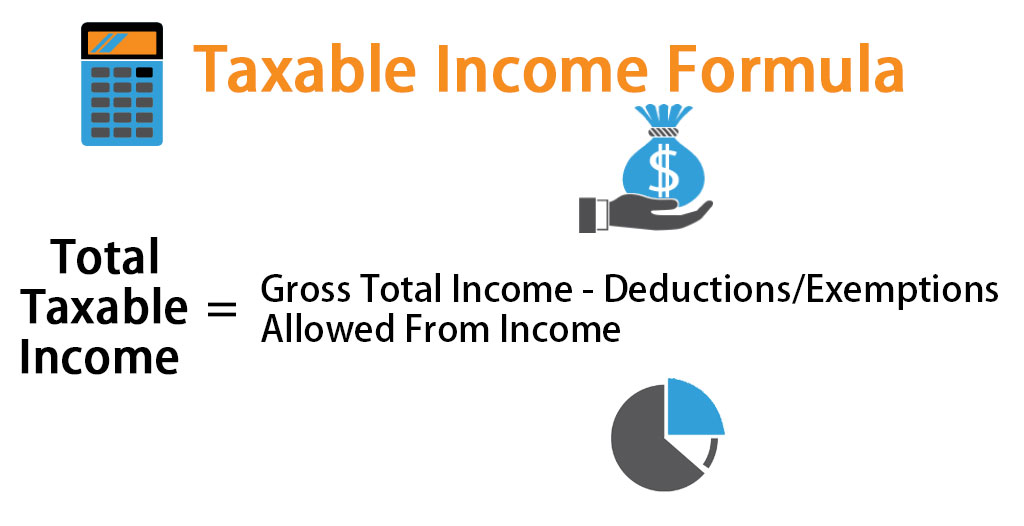

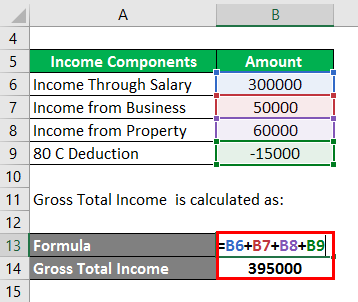

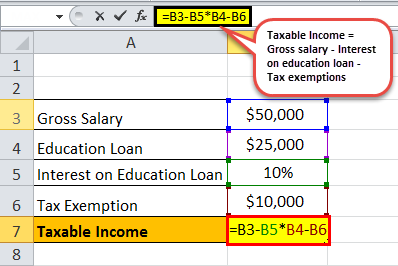

Taxable Income Formula Examples How To Calculate Taxable Income

Review the 2022 Malaysia income tax rates and thresholds to allow calculation of salary after tax in 2022 when factoring in health insurance contributions pension contributions and other salary taxes in Malaysia.

. Non-resident stays in Malaysia for less than 182 days and is employed for at least 60 days in a calendar year. Resident status and income tax in Malaysia. Residents and Non-Resident status will give a different tax regime on income earnedreceived from Malaysia.

Find Out Which Taxable Income. Restriction On Deductibility of Interest Section 140C Income Tax Act 1967 International Affairs. 21 Government grant or subsidy.

IRBM Public Key. Heres quick scenario to briefly illustrate how the whole thing works. Businesses that provide taxable goods and services must register for SST if they meet the following conditions.

An Individual will be considered Non-Resident for Income Tax purpose if the individual is physically present in Malaysia for less. So it is very important to identify whether you are Residents or Non-Resident in regard to Malaysia Tax Law. In Malaysia corporations are subject to corporate income tax real property gains tax goods and services tax GST and etc taxes.

Advance Pricing Arrangement. Find out which income can be exempted from income tax in Malaysia for 2022. Malaysia adopts a territorial scope of taxation where a tax-resident is taxed on income derived from Malaysia and foreign-sourced income remitted to Malaysia.

Directors fees income received as a non-Malaysian citizen director of a Labuan entity are exempted from income tax until YA 2025. You are non-resident under Malaysian tax law if you stay less than 182 days in Malaysia in a year regardless of your citizenship or nationality. Average Lending Rate Bank Negara Malaysia Schedule Section 140B.

Employed in Malaysia. Any individual earning more than RM34000 per annum or roughly RM283333 per month after EPF deductions has to register a tax file. For all other investment income ie interest foreign income and taxable capital gains 3067 per cent of that income is also added to the RDTOH account.

Taxable Canadian property of a taxpayer includes among other things. Non-resident corporations are subject to CIT on taxable capital gains 50 of capital gains less 50 of capital losses arising on the disposition of taxable Canadian property. 26 Year Assessment 2010 - 2014 25.

Intent is a major factor in determining whether the gain or loss is income or capital in nature. Both resident and non-resident taxpayers are taxed only on income accrued in or derived from within. You must pay income tax on all types of income including income from your business or profession employment dividends interest discounts rent royalties premiums pensions annuities and others.

Total sales value within the last 12 months exceed RM 500000. Foreigners who qualify as tax-residents follow the same tax guidelines progressive tax rate and relief as Malaysians and are. You will not be taxable if.

Your aggregate income is essentially the total of all your taxable income from employment rent royalties and so on. However foreign-sourced income of all Malaysian tax residents except for the. Ahmad has an aggregate income of RM60000 and makes a donation of RM5000 to an approved institution in March 2021.

When the corporation pays a taxable dividend to shareholders itll receive a tax refund of 1 for every 261 of dividends paid up to the balance of the RDTOH account. Which businesses must apply for sales and service tax registration in Malaysia. Rate Business trade or profession Employment Dividends Rents.

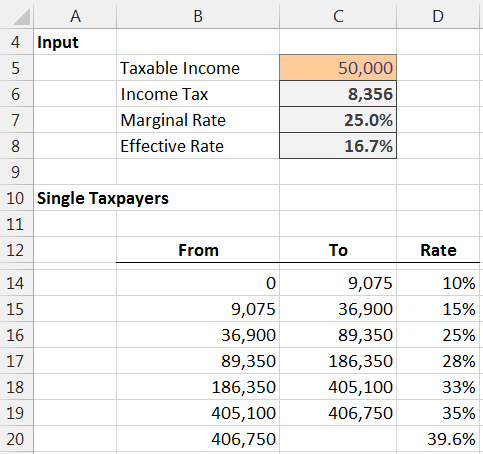

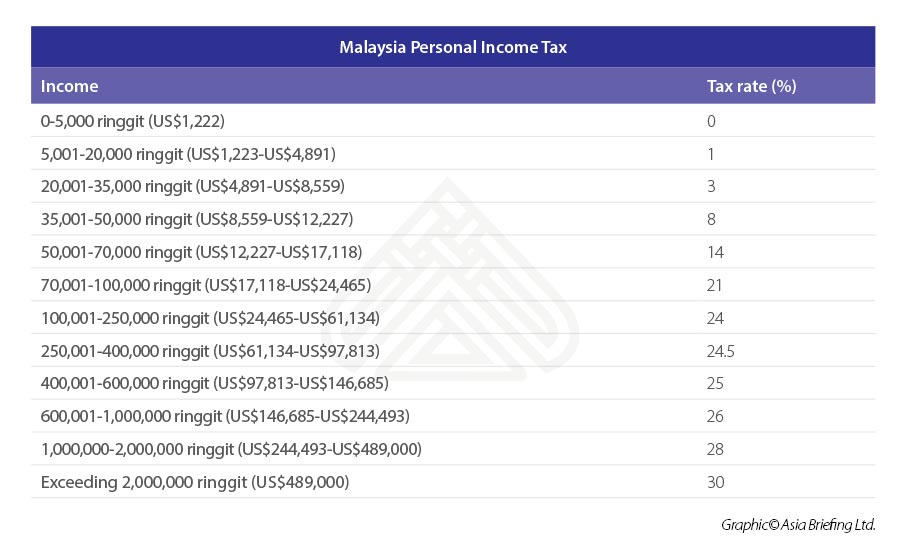

From 5000 to 20000. Estimate your take home pay after income tax in Malaysia with our easy to use and up-to-date 2022 salary calculator. Taxable Income MYR Tax Rate.

Income from RM500001. The yearly amount can be fully deducted regardless of whether the taxpayer had an income every month. The new policy will be retroactive and will apply from January 1 2020.

In other words resident and non-resident organisations doing business and generating taxable income in Malaysia will be taxed on income accrued in or derived from Malaysia. Therefore a resident taxpayer will be allowed to deduct from his taxable income US475 VND 11 million as compared to US387 VND 9 million previously.

Solved Problem 1 Hagbong Kho Corporation Has Just Completed Its Third Year Course Hero

New York State Enacts Tax Increases In Budget Grant Thornton

Guide To Tax Clearance In Malaysia For Expatriates And Locals Toughnickel

Pdf Asean Tax Malaysia Asd Dsa Academia Edu

Foreign Sourced Income Received From Outside Malaysia Tax Planning For Residents Youtube

How Is Foreign Sourced Income Taxed Thannees Articles

Income Tax Formula Excel University

Taxable Income Formula Calculator Examples With Excel Template

How Is Taxable Income Calculated How To Calculate Tax Liability

Taxable Income Formula Examples How To Calculate Taxable Income

Individual Income Tax In Malaysia For Expatriates

Taxable Income Formula Calculator Examples With Excel Template

How To Calculate Foreigner S Income Tax In China China Admissions

Taxable Income Formula Calculator Examples With Excel Template

Taxable Income Formula Examples How To Calculate Taxable Income

9 Ways To Maximise Income Tax Relief For Family Caregivers In 2022 Homage Malaysia

Taxable Income Formula Calculator Examples With Excel Template

Individual Income Tax In Malaysia For Expats Gpa

:max_bytes(150000):strip_icc()/AppleIncomeSattementDec2019-cd967d0a8f5e4748a1060f83a7e7acbc.jpg)

Net Income After Taxes Niat